But how does compound interest compare to simple interest? The critical difference is the placement of interest into the account. Under simple interest, you convert the interest to principal at the end of the transaction’s time frame.

I. Concept

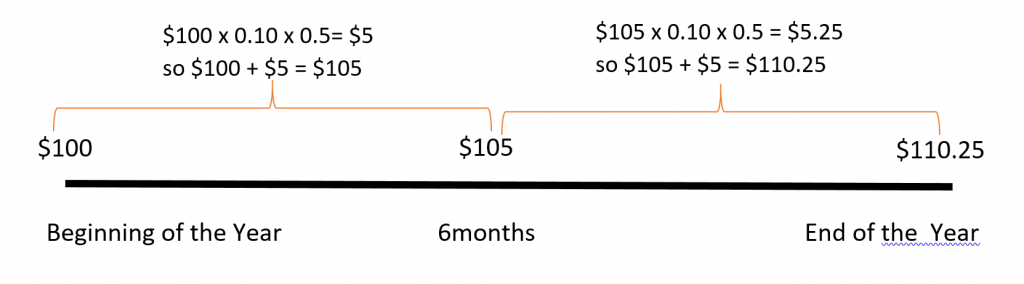

Figure 1 illustrates the process of compounding or earning interest on interest. Consider an investment of $100 that earns 10% year with interest being compounded semiannually. With semiannual compounding the interest on the investment will be calculated twice during the year.

Using the simple interest formula I = Prt, at the end of six months (half a year) interest will be calculated as follows:

I = $100 x 10% x 1/2 year = $5.

Adding this $5 to the principal of $100 you will have $105 at the end of the first six months. At the end of the year interest will be calculated again on the $105:

I = $105 x 10% x 1/2 year = $5.25.

Adding this $5.25 to $105 you will have $110.25 at the end of the year. In this case you would be earning interest not only on the original principal of $100, but also on the previously earned interest of $5. When interest is earned on interest, we say the interest is compounded. The total amount of principal and accumulated interest at the end of a loan or investment is called the compound amount.

Consider a $100 investment that earns 10%/year compounded annually. The table in Figure 2 shows how the value of the $100 investment will grow over a 6-year period.

| Year | Amount at the beginning of the year | Earned Interest | Year End Total |

|---|---|---|---|

| 1 | $100 | $10 | $110 |

| 2 | $110 | $11 | $121 |

| 3 | $121 | $12.10 | $133.10 |

| 4 | $133.10 | $13.31 | $146.41 |

| 5 | $146.41 | $14.64 | $161.05 |

| 6 | $161.05 | $16.11 | $177.16 |

Fig. 2

At the beginning of Year 1, $100 is invested, so the interest earned in the first year will be:

I = Prt = $100 × 0.10 × 1 = $10. This is added to the original $100 to result in $110 at the end of Year 1.

At the beginning of Year 2 the process will repeat but the principal P is now $110.

I = Prt = $110 × 0.10 ×1 = $11 in interest so at the end of Year 2 there will be:

$110 + $11 = $121 in the account.

Notice that the compound amount at the end of the six year period is $177.16. The investment has earned an accumulated $77.16 in interest. If the investment had earned simple interest as opposed to compound interest it would have only earned:

I = Prt = 100 × 0.10 × 6 = $60 in interest.

Compound Interest Formula

The compound interest formula is:

| where, | A = total compound amount(includes principal and interest) |

| P = principal | ||

| r = annual interest rate | ||

| n = number of times in one year that interest is calculated | ||

| t = time (in years) |

Since A includes both the principal and interest, to find the interest amount I calculate:

EXAMPLE 1

Find the compound amount and the interest earned on $100 compounded annually at 10% for 6 years.

Solution

| P = $100 r = 10% = 0.1 n = 1 (since the interest is calculated once a year) t = 6 years |

| Replace the variables with their values |

|  and and  | |

| Raise  | |

|

The interest earned is  $77.16

$77.16

The compound amount is $177.16

Interest can be compounded using a variety of compounding periods. The compounding period is the span of time between when interest is calculated and when it will be calculated again. If there is one month between every interest calculation then the compounding period is monthly. With monthly compounding there will be 12 compounding period in one year since there are twelve months in a year . The variable n in the compound interest formula reflects the number of times in one year that interest is calculated.

Compounding Periods

If interest is compounded:

annually (once per year) ⇒ n = 1

semi-annually (twice a year) ⇒ n = 2

quarterly (four times per year) ⇒ n = 4

monthly (twelve times per year) ⇒ n = 12

weekly (fifty-two times per year) ⇒ n = 52

daily (three hundred sixty-five times per year) ⇒ n = 365

EXAMPLE 2

Find the compound amount and the interest earned on $500 compounded semiannually at 6% for 3 years.

Solution

| |

|  |

(since the interest is calculated semiannually or 2 times a year) (since the interest is calculated semiannually or 2 times a year) |  |

|  |

|

The compound amount is $597.03 and the interest earned is $597.03 – $500 = $97.03

PV = Present value amount.